Recovery broadens: ChronoPulse Index rises 1.5% in May as nearly every brand gains

ChronoPulse Index rises 1.5% in May as nearly every brand gains

Johannes FörsterChrono24

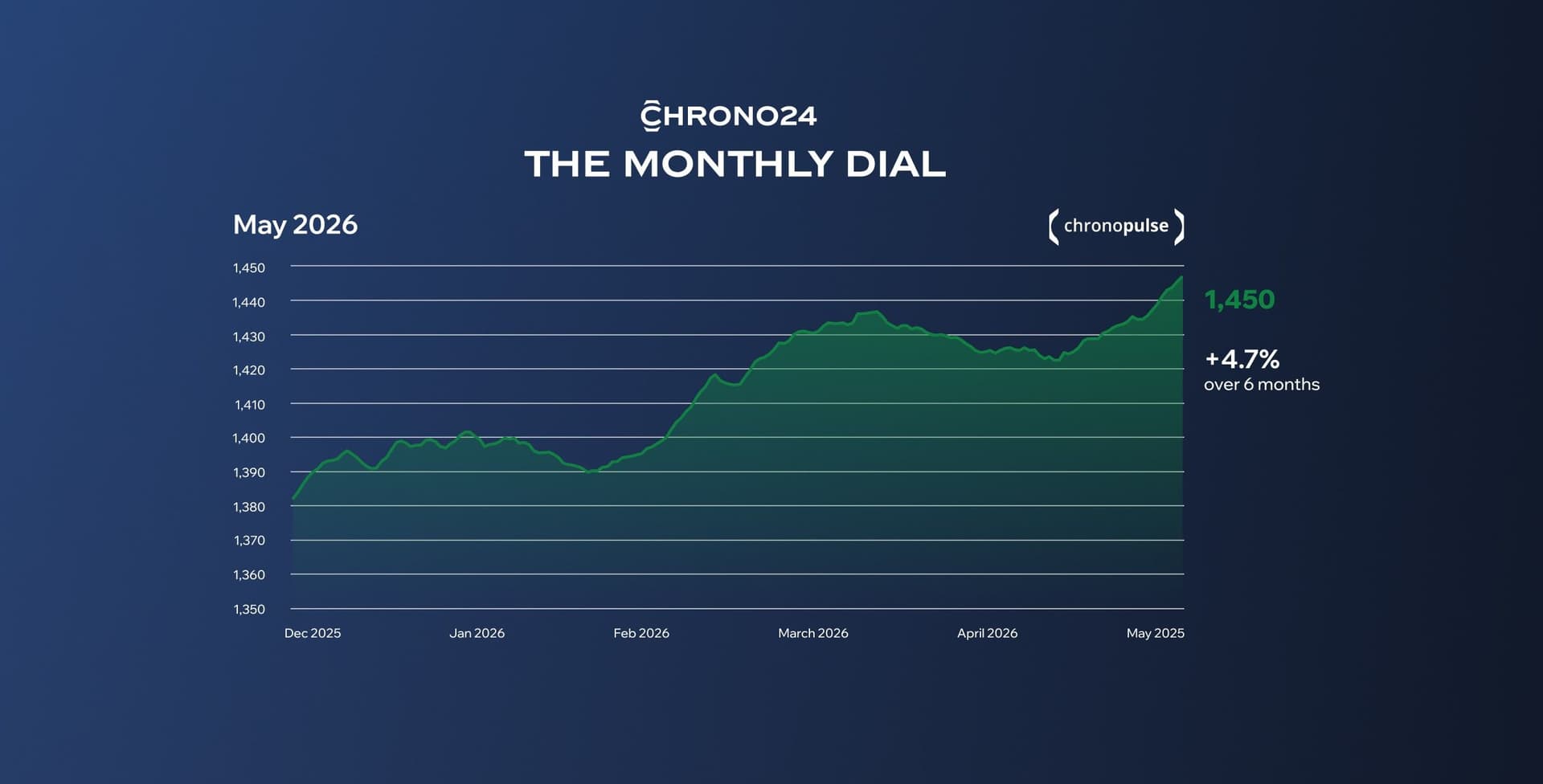

- The ChronoPulse Index rose 1.5% in May. The brands that fell hardest in April led the rebound: Vacheron Constantin swung from -5.4% to +3.3%, Cartier from -5.8% to +2.8%, Panerai from -6.4% to +2.0%.

- Breitling posted the largest single-month gain at 5.1%. Only two brands closed May lower: Omega (-0.6%) and Jaeger-LeCoultre (-0.4%).

- Over six months the index is up 4.7%, with Cartier (+6.6%), TAG Heuer (+6.3%) and Patek Philippe (+5.4%) leading the field.

Karlsruhe, June 11, 2026 – The ChronoPulse Index rose 1.5% in May. The April dip didn't last: almost every brand that gave back ground rebounded the next month. Cartier swung from -5.8% to +2.8%, Vacheron Constantin from -5.4% to +3.3%, Panerai from -6.4% to +2.0%. Breitling led the month with +5.1%, and only Omega and Jaeger-LeCoultre closed slightly lower.

Over six months the picture is steady: the index is up 4.7%, and every brand but one is in positive territory, with Cartier (+6.6%) and TAG Heuer (+6.3%) at the top. The structural backdrop holds. Retail prices at the primary market have moved higher across recent months, lifting the global reference point for new watches, and the secondary market is following. The US tariff on Swiss imports, cut from 39% to 15% and retroactive to November 2025, adds to that effect: it still raises the landed cost of a new Swiss watch in the States, which keeps the secondary market attractive.

What moved the market in May

- Cartier leads over six months (+6.6%): May's 2.8% rebound followed April's 5.8% dip, and the half-year reading is the strongest in the index. Tudor is increasingly named the value-driven alternative to Rolex, while Vacheron Constantin challenges the dominance of Patek Philippe and Audemars Piguet in the ultra-luxury segment.

- TAG Heuer is close behind (+6.3% over six months): The secondary market keeps rewarding the brand even without a recent retail increase. The 60th Anniversary Carrera, the Monaco and generally the in-house chronograph line-up are driving demand.

- Patek Philippe holds its run (+5.4% over six months): Supply contraction in Nautilus and Aquanaut references continues to support prices across the range.

- Rolex firms up (+4.5% over six months): The Pepsi GMT-Master II discontinuation at Watches & Wonders 2026 added a burst of collector interest, and demand has stayed elevated since.

The breadth of the move

Every brand but one is positive over six months. Names that recently showed weakness, including IWC, Panerai and Hublot, have all turned back up, with Hublot among the strongest gainers in May at +4.2%. Breitling's 5.1% jump was the largest of any brand in May, an early sign that its long correction may be bottoming out, though one month is not a reversal.

Balazs Ferenczi, Head of Brand Engagement at Chrono24: “The April dip didn't last. Almost every brand we track gained in May, and over six months the index is positive nearly across the board. The breadth of the move – gains across nearly every brand – points to broad-based demand rather than a narrow speculative spike."

Methodology

The ChronoPulse Index tracks price developments across 13 major luxury watch brands and 140+ model references, based on real transaction data on Chrono24's global marketplace. All percentage changes are calculated on a rolling basis. The index converts all transactions into EUR at the prevailing exchange rate at the time of the transaction. Month-over-month data for brands with lower transaction volumes can be subject to higher short-term fluctuations.

For more information: chrono24.com/chronopulse