The Monthly Dial: Recovery turns selective

ChronoPulse Index dips 0.4% in April as brands pull apart

Johannes FörsterChrono24

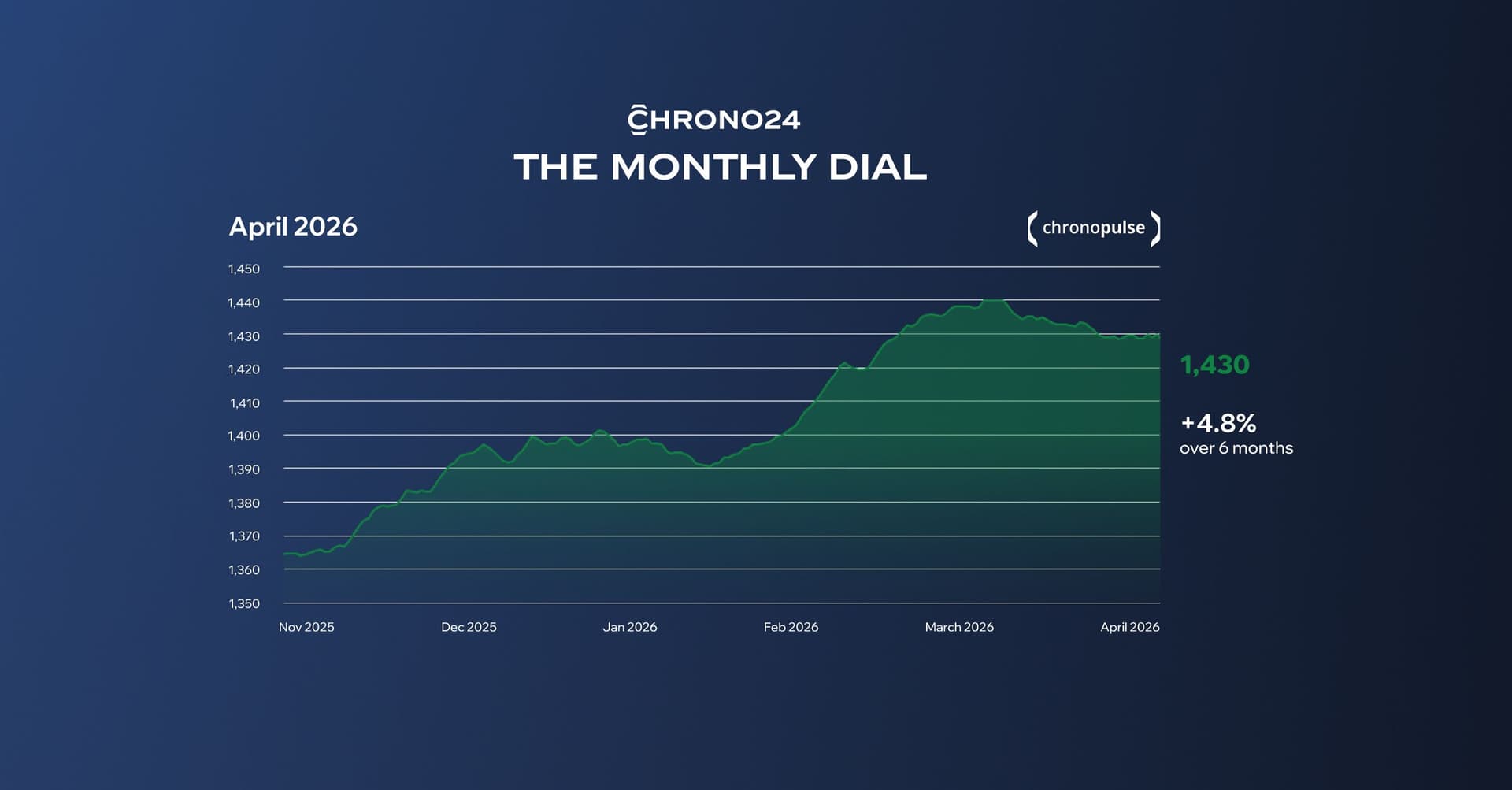

- The ChronoPulse Index slipped to 1,430 (-0.4% MoM). The 6-month trend remains intact at +4.8%.

- Patek Philippe leads the four largest brands over six months (+7.0%), while TAG Heuer is the strongest performer in the entire index (+9.0% 6M). Audemars Piguet is in negative territory (-1.4% 6M) ahead of the May 16 Royal Pop launch with Swatch.

- The Rolex GMT-Master II “Pepsi” discontinuation triggered a second demand spike of around 500% versus the 2025 weekly average on Chrono24, after a similar surge on rumor in early March. The steel reference (126710BLRO) is now up 19.7% over six months.

Karlsruhe,May 12, 2026 – After six straight months of gains, the ChronoPulse Index closed April at 1,430 (-0.4% MoM). The pullback is shallow and concentrated on the brands that gained the most in Q1: Cartier (-5.8%), Vacheron Constantin (-5.4%) and Panerai (-6.4%). The longer view is intact, with the index up 4.8% over six months and 2.1% year-on-year.

Two brands moved against the monthly trend: TAG Heuer (+3.2%) and Omega (+2.8%). Rolex held flat. Over six months, the picture broadens: TAG Heuer is now the strongest performer in the entire index (+9.0%). Among the four largest brands, Patek Philippe leads (+7.0%), ahead of Rolex (+5.5%) and Cartier (+3.9%).

Audemars Piguet sits apart from this picture. Over six months, AP is the only one of the four largest brands in negative territory (-1.4%), with the monthly (-0.8%) and yearly (-0.1%) figures both slightly down. The brand goes into the May 16 Royal Pop launch with Swatch from a position of relative weakness, which makes the collaboration's market impact one of the key questions for our next update.

What moved the market: April winners

- TAG Heuer (+3.2% MoM, +9.0% 6M) – The strongest performer in the entire index across both the monthly and six-month horizons. The breadth of the move suggests demand is broadening across the line-up rather than concentrating on a single hero reference. At a price point accessible to a wider collector base, TAG Heuer's run is the clearest signal of the market opening up beyond the top tier.

- Omega (+2.8% MoM, +3.5% 6M) – One of only two brands in positive territory in April. The 6M and YoY readings are nearly identical, signaling steady rather than accelerating demand.

- Patek Philippe (-0.7% MoM, +7.0% 6M) – Cooling slightly from the double-digit pace seen in March, but still the year's anchor. Over the past six months, all eleven Patek references in the ChronoPulse index are positive. The Aquanaut 5167A-001 is up 21% YoY, the Nautilus 5712/1A-001 gained 12.2% in the last six months alone. No other brand shows this degree of uniform appreciation across its full range.

Where the market gave back

- Panerai (-6.4% MoM, -4.7% 6M) – Weakest brand on both the monthly and six-month horizon. The sport-luxury segment outside Rolex and AP continues to lose ground.

- Cartier (-5.8% MoM, +3.9% 6M) – Gave back part of its strong Q1. The longer trend stays intact, supported by accelerating model momentum: the Santos WSSA0039 is up 19.2% 6M against only 4.6% YoY, almost all of it recent. The Tank Solo WSTA0030 reversed from -2.2% YoY to +10.5% 6M.

- Hublot (-3.2% MoM, -3.6% 6M) – Down on every horizon. Demand remains structurally weak.

- Breitling (-1.9% MoM, -1.8% 6M, -7.9% YoY) – The worst 1Y performance in the index. The mid-tier squeeze identified in March persists.

Focus: How the Pepsi reshaped Rolex's month

One watch did more to shape April than any single index movement: the Rolex GMT-Master II “Pepsi” (Ref. 126710BLRO). The discontinuation played out in two waves on Chrono24. The first hit in early March on rumor, with purchase requests roughly 500% above the 2025 weekly average and active listings down about 25%. Demand stayed at twice the 2025 average through the interim. The second wave came in mid-April when Rolex officially removed the model at Watches & Wonders, pushing requests back to 500% over the 2025 average. The official confirmation reignited buyer urgency rather than resolving it. The white gold version (Ref. 126719BLRO) shows an even sharper reaction: purchase requests up more than 700% versus the 2025 average, with listings declining steadily since the start of 2026. Volumes are lower given the higher price point, but the directional signal is the same.

The bigger picture

April marks the recovery turning selective. The brands that ran hottest in Q1 gave back part of those gains, while two brands (Omega, TAG Heuer) moved against the trend and Rolex held flat. The structural drivers are unchanged: speculators remain largely absent from the market, and US tariff dynamics continue to push buyers toward the pre-owned market. What's new in April is the spread between brands. Q1 saw most names rising together. April pulled them apart.

Looking ahead: the Royal Pop test

The May 16 Audemars Piguet x Swatch "Royal Pop" launch is the most relevant upcoming data event. Chrono24 demand for Swatch shows that the original 2022 MoonSwatch launch was by far the largest demand event on record for the brand, and that every subsequent collaboration has produced a smaller peak than the one before. The Royal Pop is the first collaboration that brings a Holy Trinity brand into the format. Whether the Royal Pop can break that pattern, and whether the original Royal Oak sees a halo effect comparable to the lift on the Speedmaster after the MoonSwatch launch, is the question we will answer in the coming weeks.

Balazs Ferenczi, Head of Brand Engagement: “The Royal Pop is not just one of the most anticipated launches of the year, it is genuinely without precedent. I cannot remember a collaboration of this kind in the industry before, with a Holy Trinity brand entering the Swatch format for the first time. The closest reference point we have is the original MoonSwatch in 2022, which lifted demand for the Omega Speedmaster Professional Moonwatch on our marketplace by around 85% in the weeks after launch. The short-term effect was clearly visible, even if a lasting structural shift is always harder to measure. With the Royal Oak, we are in entirely new territory.”

Methodology

The ChronoPulse Index tracks price developments across 14 major luxury watch brands and 140+ model references, based on real transaction data on Chrono24's global marketplace. All percentage changes are calculated on a rolling basis. The index converts all transactions into EUR at the prevailing exchange rate at the time of the transaction. Month-over-month data for brands with lower transaction volumes can be subject to higher short-term fluctuations.

For more information: chrono24.com/chronopulse