The Monthly Dial: ChronoPulse Market Update for March

ChronoPulse Market Update March 2026

Johannes FörsterChrono24

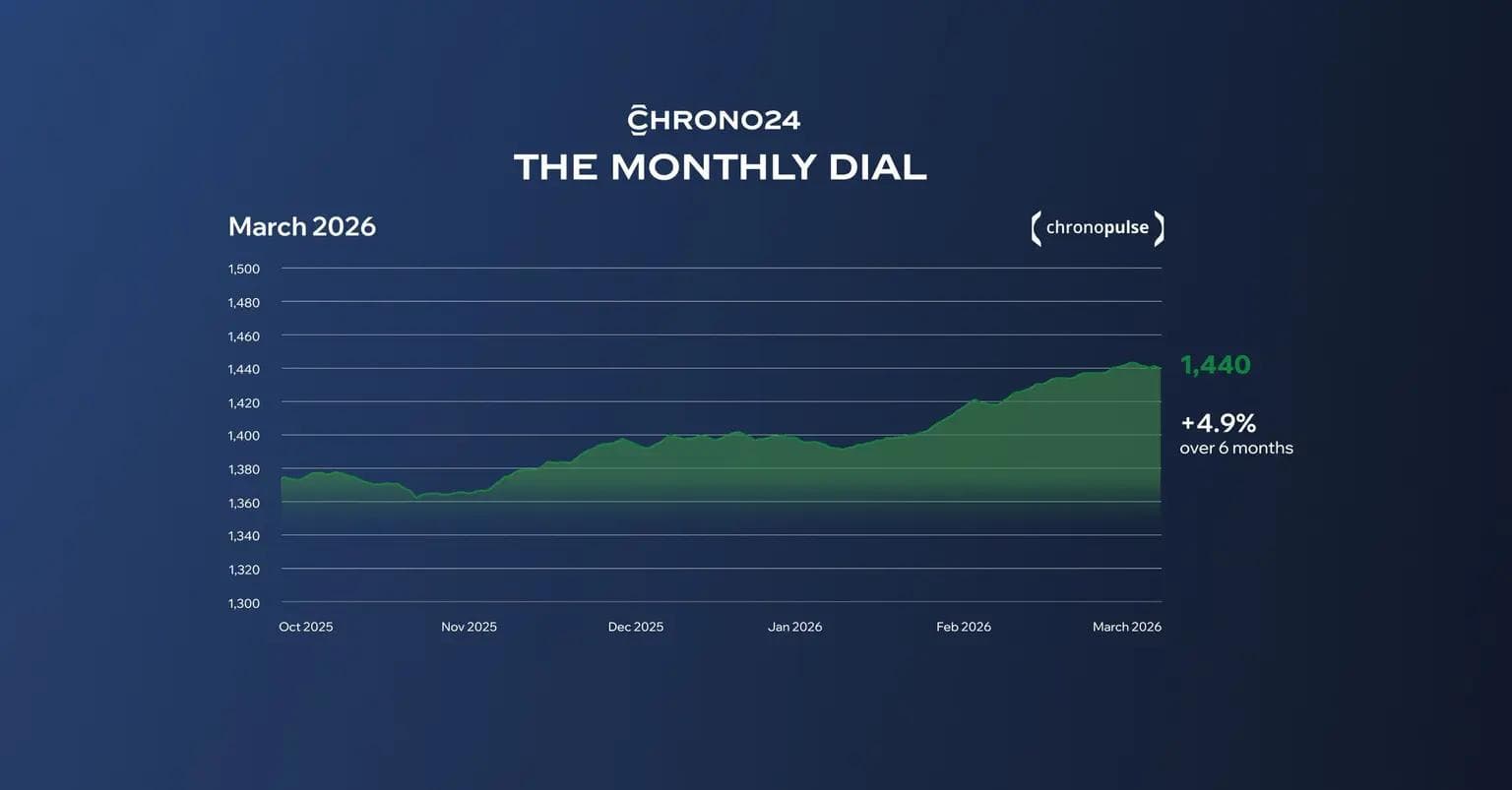

- ChronoPulse Index hits 1,440 – its highest level since April 2025. The sixth consecutive monthly gain confirms the end of a 13-quarter correction.

- Patek Philippe and Cartier lead the recovery with double-digit 6-month gains above 10%, driven by genuine collector demand rather than speculation.

- Capital is shifting toward heritage and haute horlogerie, while mid-tier brands grow below market average – signaling a deeper structural realignment.

Karlsruhe, April14, 2026 – The ChronoPulse Index closed March at 1,440, its highest level since April 2025. The market has now gained steadily for six consecutive months following the technical floor reached in August 2025. With speculators largely gone and collector-driven demand setting the pace, the recovery is broadening across nearly all index brands – a pattern not seen in over three years. Meanwhile, the introduction of 39% US import tariffs on Swiss watches continues to redirect buyer interest toward the secondary market, adding further momentum to the upturn.

Brand Performance: What moved the market

- The recovery is accelerating. The 6-month gain of +4.9% is driven by real collector demand, not speculation. All but one brand in the index posted positive 6-month growth.

- Patek Philippe and Cartier lead the field. Both posted double-digit 6-month gains (+10.7% and +10.5% respectively), confirming a sustained shift toward heritage and haute horlogerie.

- Rolex normalizes in the midfield. At +3.8% over six months, Rolex is growing in line with the broader market but is no longer the volatile outlier it was during the pandemic years.

The bigger picture

The current ChronoPulse level of 1,440 marks the end of a 13-quarter downturn that began at the market's all-time high in March 2022. Since bottoming out on August 13, 2025, the index has recovered by approximately 5.9%.

Two structural factors are supporting the recovery. First, the speculative "flippers" who drove the 2021/2022 price bubble have largely exited the market. Current price gains are supported by actual collector demand. Second, the implementation of 39% US import tariffs on Swiss watches in August 2025 made secondary market supply a more attractive alternative to rising retail prices, particularly in the US.

The broader trend is clear: capital is rotating from mid-tier brands toward the higher end (Cartier, Patek Philippe, Vacheron Constantin), while several established brands in the mid-price segment are growing below the market average, reflecting a broader structural shift.